The IRS penalty for late filing can significantly increase the amount of tax you owe if your tax return is filed after the deadline. Many taxpayers are unaware that failing to file a return on time may trigger penalties that grow quickly over time.

The IRS imposes late filing penalties to encourage taxpayers to submit their returns by the annual tax deadline. Even if you cannot pay your tax balance immediately, filing your return on time can help you avoid some of the most expensive penalties.

This guide explains how the IRS penalty for late filing works, how much the IRS charges, and what steps you can take to reduce or avoid these penalties.

What Is the IRS Penalty for Late Filing?

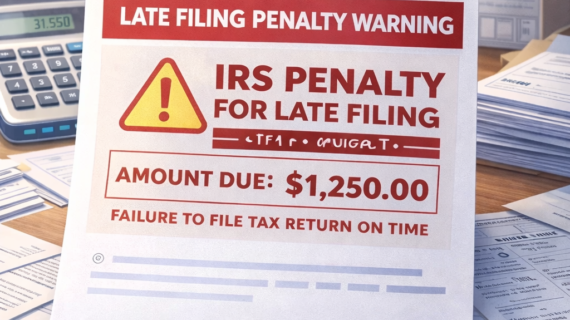

The IRS penalty for late filing, also known as the failure-to-file penalty, is charged when a taxpayer does not submit their federal tax return by the deadline.

The standard tax filing deadline is usually April 15 each year. If a taxpayer fails to file their tax return by that date and does not request an extension, the IRS may assess a late filing penalty.

The penalty continues accumulating each month until the tax return is filed.

How the IRS Calculates Late Filing Penalties

The IRS penalty for late filing is typically calculated as a percentage of the unpaid tax balance.

The standard penalty rate is:

- 5% of the unpaid tax per month

- Maximum penalty of 25% of the unpaid tax

If the tax return is more than 60 days late, the IRS may apply a minimum penalty amount.

Difference Between Late Filing and Late Payment Penalties

Many taxpayers confuse the IRS penalty for late filing with the penalty for late payment. Although both penalties apply to unpaid taxes, they are calculated differently.

Late Filing Penalty

The failure-to-file penalty applies when a taxpayer does not submit their tax return by the deadline.

Late Payment Penalty

The failure-to-pay penalty applies when a taxpayer files a return but does not pay the full balance owed.

Both penalties may apply simultaneously if a taxpayer neither files nor pays their taxes on time.

How Quickly Late Filing Penalties Grow

The IRS penalty for late filing grows quickly because it is calculated monthly.

For example:

- Month 1: 5% penalty

- Month 2: additional 5%

- Month 3: additional 5%

- Maximum penalty: 25%

This means a taxpayer who owes $10,000 in taxes could face a penalty of $2,500 simply for filing late.

When the IRS Sends Notices About Late Filing

If a taxpayer fails to file their return or pay taxes owed, the IRS will usually send a series of notices.

Many taxpayers first receive the IRS CP14 notice explaining unpaid tax balances.

If the balance remains unpaid, the IRS may send reminder letters such as the IRS CP501 notice explaining tax balance reminders.

Ignoring these notices may lead to additional warnings such as the IRS CP504 notice warning about levy action.

What Happens If You Ignore Late Filing Penalties

If taxpayers ignore IRS penalties, the situation can escalate.

Penalties and interest continue accumulating while the IRS continues sending collection notices.

In severe cases, the IRS may begin collection actions such as wage garnishment or bank levies.

Our guide explaining what happens if you ignore IRS notice letters provides more details about these risks.

How To Avoid the IRS Penalty for Late Filing

File Your Tax Return on Time

The easiest way to avoid the IRS penalty for late filing is simply filing your tax return before the deadline.

Request a Tax Filing Extension

Taxpayers who need additional time can request an extension, which allows them to file their return later without triggering the late filing penalty.

However, an extension does not extend the payment deadline.

Pay Taxes Owed as Soon as Possible

Even if you cannot pay the full balance, submitting a partial payment may reduce penalties.

Options If You Cannot Pay Your Taxes

IRS Installment Agreement

An installment agreement allows taxpayers to pay tax debt through monthly payments.

Learn more in our guide explaining IRS installment agreement requirements.

Offer in Compromise

Some taxpayers may qualify to settle their tax debt for less than the full balance.

Currently Not Collectible Status

If taxpayers experience financial hardship, the IRS may temporarily suspend collection actions.

Penalty Relief Options

The IRS offers several programs that may allow taxpayers to remove or reduce penalties.

First-Time Penalty Abatement

Taxpayers with a clean filing history may qualify for penalty relief.

Reasonable Cause Relief

The IRS may remove penalties if taxpayers demonstrate a valid reason for filing late.

Frequently Asked Questions

What is the maximum IRS late filing penalty?

The maximum penalty is typically 25% of the unpaid tax balance.

Can the IRS remove late filing penalties?

Yes, taxpayers may qualify for penalty abatement under certain conditions.

What if I cannot pay my taxes?

You should still file your return on time and explore payment plan options.

Conclusion

The IRS penalty for late filing can increase your tax debt quickly if you fail to submit your tax return by the deadline. Understanding how the penalty works can help you avoid unnecessary charges.

Filing your tax return on time, requesting extensions when necessary, and communicating with the IRS are the best ways to avoid late filing penalties.