The IRS failure to pay penalty is one of the most common penalties imposed on taxpayers who do not pay their taxes on time. While many people focus on filing their tax return, failing to pay the balance owed can quickly lead to growing penalties and interest.

Even if you file your tax return on time, the IRS may still charge penalties if you do not pay the full amount owed by the deadline. Over time, these penalties can significantly increase your total tax debt.

This guide explains how the IRS failure to pay penalty works, how much it costs, how it grows over time, and how you can reduce or avoid it.

According to the IRS official penalties page, penalties apply when taxpayers fail to meet payment deadlines or comply with tax obligations.

What Is IRS Failure To Pay Penalty?

The IRS failure to pay penalty is a charge applied when a taxpayer does not pay the full tax amount owed by the due date.

This penalty applies even if the taxpayer has already filed their tax return.

IRS Failure To Pay Penalty Rate

The standard IRS failure to pay penalty rate is:

- 0.5% of unpaid tax per month

- Maximum penalty of 25%

This penalty continues until the balance is paid in full.

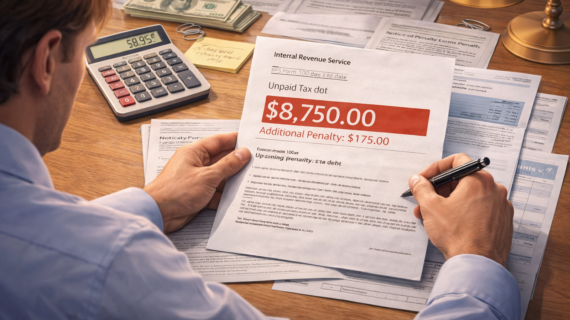

How IRS Failure To Pay Penalty Grows Over Time

The IRS failure to pay penalty accumulates monthly, making unpaid tax debt grow steadily.

Example Calculation

If you owe $10,000 in taxes:

- Month 1: $50 penalty

- Month 6: $300 penalty

- Month 12: $600 penalty

Interest is also added, increasing the total amount owed.

Difference Between Failure To Pay and Failure To File

- Failure to file: 5% per month

- Failure to pay: 0.5% per month

The failure to file penalty is much higher, so filing on time is critical.

See IRS late filing penalty explained.

When the IRS Starts Charging Penalties

The IRS begins charging penalties immediately after the tax deadline if payment is not made.

IRS Notice Process for Unpaid Taxes

The IRS sends multiple notices before taking action:

- CP14 – initial notice

- CP501 – reminder

- CP503 – urgent notice

- CP504 – levy warning

See IRS CP504 notice explained.

What Happens If You Ignore the Penalty

If ignored, penalties continue growing and may lead to:

- Wage garnishment

- Bank levy

- Tax lien

How To Reduce IRS Failure To Pay Penalty

Pay As Much As Possible

Partial payments reduce penalties.

Set Up Payment Plan

See IRS installment agreement.

Request Penalty Abatement

Penalty Relief Options

- First-time penalty abatement

- Reasonable cause relief

See IRS first time penalty abatement.

How To Avoid IRS Failure To Pay Penalty

- Pay taxes before deadline

- File returns on time

- Set up payment plan early

Frequently Asked Questions

Is failure to pay penalty avoidable?

Yes, by paying on time or arranging payment plan.

Can IRS waive the penalty?

Yes, through abatement programs.

Does interest apply?

Yes, interest applies in addition to penalties.

Conclusion

The IRS failure to pay penalty can significantly increase your tax debt over time. Understanding how it works helps you take action early and avoid unnecessary costs.

Paying taxes on time, setting up payment plans, and requesting penalty relief can help reduce financial stress and prevent further IRS actions.