The IRS interest and penalty calculation determines how quickly your tax debt increases when you fail to pay taxes on time. Many taxpayers are surprised to learn that penalties and interest continue to grow daily, making even a small tax debt much larger over time.

If you owe taxes and delay payment, the IRS applies both penalties and interest until the full balance is paid. Understanding how IRS interest and penalty calculation works can help you reduce costs and avoid long-term financial problems.

This guide explains how the IRS calculates interest and penalties, how much they can add to your debt, and what steps you can take to minimize these charges.

According to the IRS official interest page, interest compounds daily on unpaid taxes and penalties.

What Is IRS Interest And Penalty Calculation?

The IRS interest and penalty calculation is the method used by the IRS to determine how much additional money you owe when taxes are unpaid or filed late.

This calculation includes:

- Late payment penalties

- Late filing penalties

- Daily interest charges

Types of IRS Penalties Included

Failure To Pay Penalty

Applies when taxes are not paid on time.

See IRS failure to pay penalty explained.

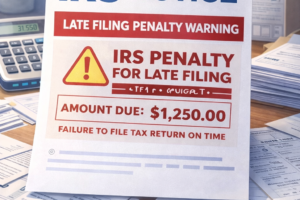

Failure To File Penalty

Applies when tax return is filed late.

Underpayment Penalty

Applies when estimated taxes are too low.

How IRS Interest Is Calculated

IRS interest is calculated daily based on the federal short-term rate plus an additional percentage.

Key Points

- Interest compounds daily

- Rates change quarterly

- Applies to both tax and penalties

How Penalties Are Calculated

Failure To Pay

- 0.5% per month

- Max 25%

Failure To File

- 5% per month

- Max 25%

Combined penalties can increase quickly if both apply.

Example of IRS Interest And Penalty Calculation

Suppose you owe $10,000:

- Failure to pay: $50/month

- Failure to file: $500/month

- Interest added daily

After several months, total debt may exceed $13,000.

Why IRS Debt Grows So Fast

The combination of penalties and daily interest causes rapid growth.

Even small delays can significantly increase total debt.

IRS Notice Sequence and Growing Debt

- CP14 – initial notice

- CP501 – reminder

- CP503 – urgent notice

- CP504 – levy warning

- LT11 – final notice

Ignoring notices leads to enforcement actions.

See what happens if you ignore IRS notices.

How To Reduce IRS Interest And Penalties

Pay as Soon as Possible

Reduces total charges.

Set Up Payment Plan

See IRS installment agreement.

Request Penalty Abatement

See remove IRS penalty.

Offer in Compromise

See offer in compromise.

Can IRS Interest Be Removed?

Interest is rarely removed unless penalties are reduced.

How To Avoid IRS Interest And Penalties

- File on time

- Pay taxes early

- Estimate taxes correctly

Real-Life Scenario

A taxpayer delayed paying $5,000 in taxes for one year. With penalties and interest, the total increased to over $6,500.

Frequently Asked Questions

Does IRS interest stop?

Only when tax is fully paid.

Can penalties be removed?

Yes, through abatement.

Is IRS interest high?

It compounds daily, making it significant over time.

Conclusion

The IRS interest and penalty calculation can significantly increase your tax debt if not managed properly. Understanding how these charges work allows you to take action early and reduce financial impact.

By paying on time, using payment plans, and requesting relief when eligible, you can minimize penalties and interest.